Benefits adjustments*

Age 62: Reduced benefits = negative 30%.

Full Retirement Age (Age 67) = 100%

Age 70: Increased benefits = 24%.

Your priorities — and spending — will likely change as you move through retirement. Here’s how to prepare.

Traveling? Volunteering? Spending more time with loved ones? You probably have an idea of what you will do in your perfect retirement. But don’t count on it staying the same over what could be a period of more than 30 years. Your retirement will evolve over time. Most people go through three stages of retirement: exploring, nesting and reflecting.

In the first stage of retirement, while your health is good and you have goals to accomplish, you might travel the world, learn new skills, volunteer and take up new hobbies. Move to a new locale and/or purchase a second home. Perhaps even start a new business or work part-time.

Your key financial priorities will be to continue to invest for growth and future healthcare costs, while also funding increased spending to pursue your goals.

Once you stop receiving a regular paycheck, you will move from accumulating assets for retirement to decumulating your assets in retirement. In the same way it was important to have a plan to build up your assets, you will need a plan to draw down your assets.

You’ll want to ensure you have a predictable income stream that covers both your essential and discretionary expenses.1 This will most likely include income from a combination of Social Security benefits, pensions and annuity payments and withdrawals from IRAs, 401(k)s and personal investment accounts. Your advisor, along with your tax professional, will help you develop a withdrawal strategy that can address your income needs and also take your taxes into consideration.

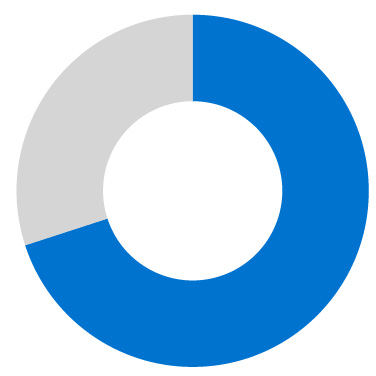

Sources of income among retirees (65+)2 | |

92% | Social Security |

65% | Pension |

47% | Interest, dividends or rental income |

25% | Wages, salaries or self-employment |

5% | Cash transfers, other than Social Security |

Note: Among retirees. Respondents could select multiple answers. Sources of income include the income of a spouse or partner. | |

Part of your income stream in retirement will no doubt come from your Social Security benefits, which you can begin receiving as early as age 62. Or you may want to defer taking those benefits until you reach full retirement age or even age 70 (at which time your benefit amount will be capped).

Full Retirement Age determination* | |

Birth year | Full Retirement Age |

1937 or earlier | 65 |

1938 – 1942 | 65 + 2 months per year after 1937 until 1943 |

1943 – 1954 | 66 |

1955 – 1959 | 66 + 2 months per year after 1954 until 1960 |

1960 or later | 67 |

At what age you begin taking your Social Security benefits will depend on your personal needs and anticipated lifespan.3 It is an important decision and should be discussed with your advisor as you develop your plan for funding your retirement expenses.

Healthcare costs in retirement are usually more than most people anticipate. Premiums, out-of-pocket expenses and critical services not covered by Medicare can deplete your retirement savings if you aren’t prepared for them.

In fact, a healthy 65-year-old couple who retired in 2023 will likely use nearly 70% of their lifetime Social Security benefits to cover their medical costs in retirement.4 You can use this time in the early phase of your retirement to make sure your projected healthcare budget is sufficiently addressed to help you cover the healthcare costs you will incur in the later stages of retirement.

70%

of lifetime Social Security benefits will likely be used to cover medical costs in retirement for a 65-year-old couple who is healthy in 2023.4

By extending the time you remain in the workforce, you may be able to continue to fund your retirement without taking early Social Security benefits and/or withdrawals from your retirement accounts. Because we are living longer and healthier lives, this is an option for more and more retirees.

According to the U.S. Bureau of Labor Statistics, by 2032, 8.6 percent of the civilian labor force is projected to be older than 65. In fact, older adults are one of two age groups expected to increase their labor force participation over the decade. By 2032, 21 percent of older adults will be in the labor force.5

In the next stage, when you are less active, you may settle into a routine with a more relaxed pace or travel closer to home visiting friends and family. Or perhaps relocate or downsize your home.

As your spending slows a bit, consider using this period to prepare for potentially higher expenses in the next stage that could be the result of inflation and rising healthcare costs.

A 65-year-old woman invested in all bonds would have an 82% probability of not outliving her wealth. If she was invested in 50% bonds and 50% cash, that probability would increase to 97%.6 It’s important to align your investment strategy to help ensure your money lasts throughout your lifetime.

1/3 of homeowners between ages 77 and 97 who recently purchased a new home did so to be close to family or friends.7 If you’re considering relocating to another state, it’s important to understand the tax implications. If you decide to stay put, consider the cost of renovations that may be needed to help you safely and comfortably age in place.

People turning 65 today have almost a 70% chance of needing some type of long-term care.8 And Medicare generally doesn’t cover the cost of that care. You don’t want to burden your children with caregiving responsibilities or ask them to help you pay for professional care. Remember to plan ahead, whether that’s deciding to self-fund or getting long-term care insurance.

In this stage, when you may be facing lifestyle challenges such as encountering more health-related expenses, becoming a widow or widower, or needing support from your family or others. You may also start thinking more deeply about your estate plan.

You may want to strike a balance between securing your own financial future and leaving a legacy.

While Medicare covers in-home hospice care at the end of life, someone turning 65 today has an almost 70% chance of needing long-term care.8 The financial impact can be significant, even for occasional assistance in your home. Planning for those costs ahead of time can help you have the resources in place before you need them.

Avoid burdening your family. Documents such as a will, power of attorney and healthcare directive should be reviewed more often as you age to address any changes in your health and/or relationships.

You should also review your account beneficiaries once a year, or whenever you have a significant life-changing event.

1/4 of Americans say inflation has caused them to see a greater need for estate planning.9 Gifting assets while you are still alive can potentially decrease the size of your estate and therefore the amount of estate taxes. Gifting can also be personally rewarding as you have the opportunity to witness how your assets can benefit friends and family while you are still alive.

Depending on when you retire, your goals in retirement and the state of your health, you may find that you will experience all three stages of retirement — or you may only experience one or two of them. Each stage will impact your expenses and, therefore, will be important in determining your retirement income needs.

The more you can envision your plans for retirement, and the earlier you can do that, the better your chances will be for making them happen.

All our advisors are committed to putting your needs and priorities first. Find some who match your personal preferences too.

* Social Security Administration Publication EN 05-10035 Social Security Retirement Benefits, 2023.

1 Merrill. "How will you replace your salary when you retire?" Published January 2025.

2 Board of Governors of the Federal Reserve System. “Economic Well-Being of U.S. Households in 2022,” May 2023.

3 Merrill. "When and how to claim Social Security." Published September 2025.

4 HealthView Services. “Medicare and Social Security COLAs: Putting the 2023 Numbers into Context,” October 2023.

5 Pew Research Center. “Older workers are growing in number and earning higher wages,” December 14, 2023.

6 Merrill. "3 Steps to help your money last in retirement." Published May 2025.

7 National Association of Realtors®. “Home Buyers and Sellers Generational Trends Report,” 2023.

8 Merrill. “Long-term care insurance.” Published October 2025.

9 Lustbader, R. “2024 Wills and Estate Planning Study.” Caring.com. Accessed January 31, 2024.

Merrill, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

This material should be regarded as educational information on healthcare considerations and is not intended to provide specific healthcare advice. If you have questions regarding your particular situation, please contact your legal or tax advisor.

Long-term care insurance coverage contains benefits, exclusions, limitations, eligibility requirements, and specific terms and conditions under which the insurance coverage may be continued in force or discontinued. Not all insurance policies and types of coverage may be available in your state.

Consider these helpful tips for every stage of your retirement journey.

Then we can provide you with relevant answers.

Get started