Market briefs

Breaking insights on the economy, market volatility, policy changes and geopolitical events

Q2 earnings point to potential market opportunities

COULD INVESTORS BE IN FOR A BIG LETDOWN after a torrid first quarter for S&P 500 corporate earnings? Not according to Wall Street analysts, who project 20%-plus second-quarter year-over-year growth1 as Q2 earnings roll in through late August.

“Two straight quarters of better than 20% growth is a high bar,” says Lauren J. Sanfilippo, senior investment strategist in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. “But U.S. companies continue to find ways to grow earnings.” In a recent CIO Capital Market Outlook article, “A high hurdle for Q2 earnings,” she examines what’s behind this remarkable streak and what it might mean for investors moving forward.

4 good reasons for investor confidence

Though past performance is no guarantee of future results, the following statistics paint a picture of broadening market participation, says Sanfilippo.

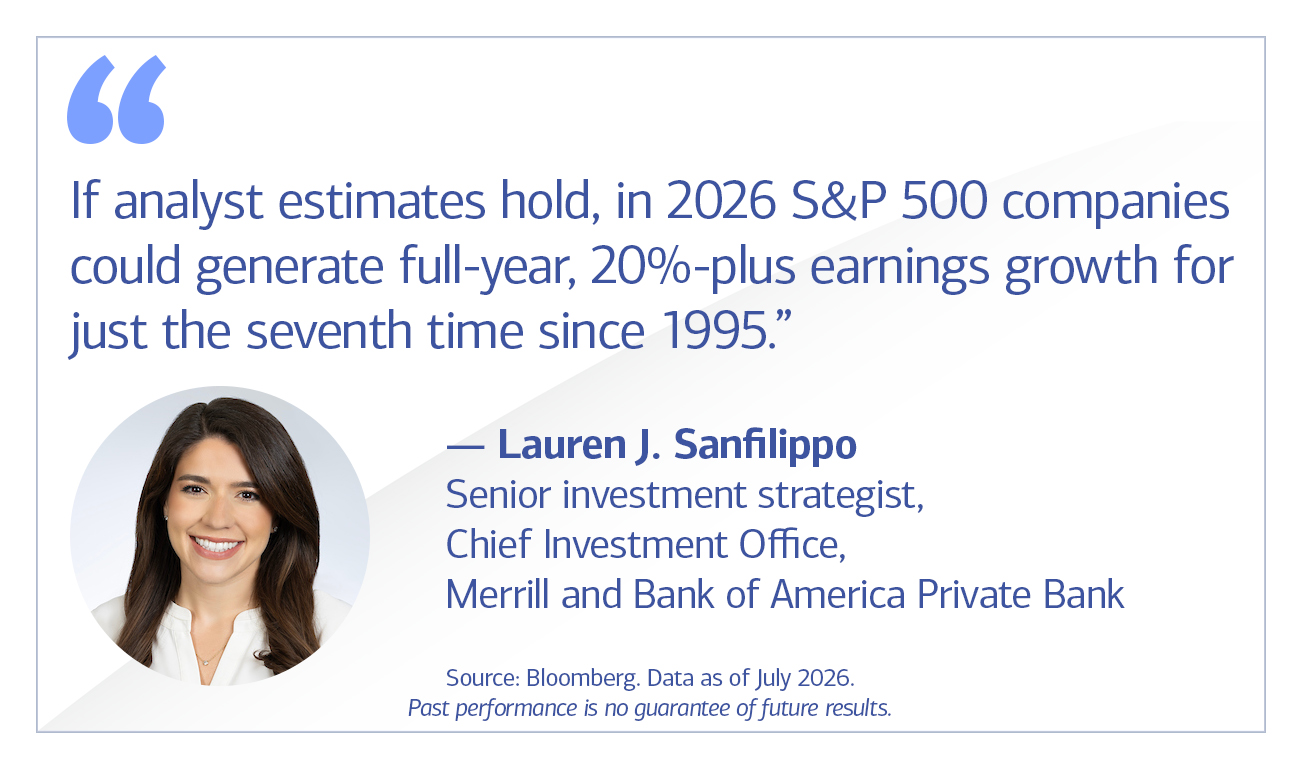

- If analyst estimates hold, in 2026 S&P 500 companies could generate full-year, 20%-plus earnings growth for just the seventh time since 1995.2

- Even more encouraging is the breadth of industries taking part. “All but one sector are expected to report positive Q2 earnings,” she says.3

- Stock performance has similarly broadened. While the “Magnificent Seven” tech giants rose 5.5% through mid-July, the rest of the index, “the S&P 493,” rose 14%.4

- As of mid-July, more than 60% of S&P 500 stocks were trading above their 50-day moving average, and nearly 15 were up more than 100%.5

Consider using the broadening market to increase diversification

“The high level of earnings growth and improving market breadth reinforces the case for portfolio diversification,” Sanfilippo believes. “Sectors such as financials, healthcare and consumer staples in particular have benefited from the rotation away from a handful of mega technology stocks.” Of course, conditions can change unexpectedly, but market unpredictability also argues in favor of a portfolio diversified across and within asset classes, she notes.

What’s next in Q3?

Can this earnings pace continue, and what are the risks to watch out for? Be sure to catch Sanfilippo’s Q3 conversation with Chief Investment Officer Chris Hyzy, “Four for the Quarter: Top questions investors are asking right now,” for more insights on shifting equity market leadership, fixed income trends and portfolio strategy considerations.

As always, tune in to the CIO’s Market Update audiocast series to follow latest market developments.

Fed doesn’t budge on rates: What it means for you

THE FEDERAL RESERVE (THE FED) ON JULY 29 kept its federal funds rate at 3.50% to 3.75%. While rate expectations have broadly shifted from cuts to potential increases later this year, the Fed so far this year has held steady as it processes complex and sometimes mixed signals on the economy and inflation.

What’s next for interest rates?

Testifying before Congress on July 14, new Fed Chair Kevin Warsh underscored the Federal Open Market Committee’s commitment “to put these years of high inflation behind us.”1 With the Iran war elevating energy costs and U.S. companies and consumers showing remarkable resilience, many analysts believe the Fed will soon raise rates to keep inflation from reigniting. BofA Global Research now expects three rate increases of .25% each in 2026, starting in September.

Yet the Fed still faces a delicate balance. Lower-than-expected inflation2 and employment figures3 from June offered reminders of early 2026, when a seemingly slowing economy raised expectations of a cut. “Further rate decisions will be based on the Fed’s analysis of the latest information as it unfolds,” says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank.

How can investors manage rate uncertainty?

“A period of higher rates, if it happens, could add income potential for bond investors, while making borrowing for large purchases more expensive,” Hyzy notes. “But keep in mind that, wherever rates head next, one of the best ways to prepare is a well-diversified portfolio designed to pursue your personal goals.”

Check back here for updates on interest rates and markets, and tune in regularly to the Market Update audiocast for latest insights from the Chief Investment Office.

1The Federal Reserve, “Semiannual monetary policy report to the Congress,” July 14, 2026.

2The Wall Street Journal, “Inflation slowed to 3.5% in June, as Americans got a break from gasoline prices,” July 14, 2026.

3CBS News, “Employers added 57,000 jobs in June, far below forecasts as hiring slowed,” July 2, 2026.

Ready to get started now? We are, too.

A banner year for IPOs: What investors need to know

A WAVE OF HIGH-PROFILE INITIAL PUBLIC OFFERINGS (IPOs) has generated excitement for many investors in 2026, and for good reason. The three largest planned offerings (one launched in June) have a combined market value estimated at $3 trillion or more,1 and a host of smaller offerings are also anticipated this year.

“Investors who have never participated in an IPO may be wondering whether and how to buy in,” says Joe Quinlan, head of Market Strategy in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. A recent CIO Capital Market Outlook article, “Mega IPOs,” explores what to expect. Here, Quinlan answers some of your questions.

What’s driving the IPO wave?

Many are in areas like space or artificial intelligence — expensive propositions requiring money for growth. There are trillions of dollars of capital ready to be put to work and an accommodating regulatory and policy environment. It adds up to favorable IPO conditions right now.

How (and when) can I invest in an IPO?

Investors can buy individual shares through public markets once an IPO occurs. If you believe in a company’s story and potential, this is a more direct approach than gaining exposure through a mutual fund or exchange-traded fund (ETF), whose many holdings dilute exposure to any one company.

For qualified investors, private equity or venture capital funds may offer access at the initial asking price, before the IPO occurs and public investors potentially drive the price up. These strategies vary and carry risks beyond the IPO’s performance, so investigate fully before investing.

What should I consider before investing in an IPO?

While initial buzz can drive share prices higher out of the gate, IPOs often need time to find their footing as public companies. They’re generally considered a long-term investment by investors seeking growth — and that growth can take time to develop. In the meantime, expect some volatility, especially in the first few months to a year, when “lock-up” restrictions end. This could add more supply to the market, which could create some temporary pressure from time to time.

How could IPO volatility affect my other investments, including index funds in my portfolio?

The U.S. has a long record of incubating companies, taking them public and absorbing them into the equity markets. Consider the impact of the 10 largest IPO companies launched between 1969 and 2012 and currently on the S&P 500: the total returns of the S&P 500 averaged 19% a year after the IPOs’ launch and 33% after two years.2

In the short term, we believe the impact of volatility will also be milder than media attention suggests. Even though recently some indexes have begun approving IPOs for inclusion as soon as five, 10 or 15 days after listing, rather than the usual three to 12 months, the initial floats, or number of shares open to the public, of the largest IPOs will likely total just 3% to 10% of the companies’ total market capitalization. Since many major indexes base inclusion on float size rather than total size, the IPOs’ initial effect on index value should be comparatively modest.

The bottom line

As with any investment, consider your overall strategy and objectives, and keep in mind that many investors view IPOs as part of a long-term investment strategy. Take a look at the existing balance of growth versus value stocks in your portfolio and ask yourself: Do you need more exposure to growth stocks? If so, an IPO could be a potential opportunity to consider. If you work with an advisor, they can help you decide whether an IPO makes sense for your situation and how to position your portfolio to remain properly balanced across and within asset classes.

For a more in-depth look at IPOs and their impact on the markets, read “Mega IPOs.” And tune in regularly to the CIO Market Update audiocast for timely insights on the economy and markets.

1Reuters, “Biggest IPO wave in history promises $3 trillion in value,” April 23, 2026.

2Bloomberg. Data as of June 30, 2026.

Securities issued in IPOs have no trading history, and information about the companies may be available for very limited periods. Prices of securities issued in IPOs may be highly volatile, and such investments may result in increased transaction costs and expenses. An investor may lose all or part of the investment in an IPO if the issuing company fails to achieve a certain level of market capitalization.

Alternative investments are intended for qualified investors only. Alternative Investments such as private equity and venture capital funds can result in higher return potential but also higher loss potential.

The United States: Most successful startup ever?

IN NEARLY 1,400 WORDS, THE DECLARATION OF INDEPENDENCE never uses the terms “business,” “entrepreneur” or “capital investment.” “Yet the founders in 1776 didn’t just declare national sovereignty. They unleashed the greatest startup in history—the U.S. economy,” says Joe Quinlan, head of Market Strategy for the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank.

“Despite headline-grabbing challenges, the U.S. remains the world’s biggest economic engine and most dynamic entrepreneurial culture,” notes Quinlan, co-author of a recent CIO Capital Markets Outlook report, “America at 250.” The report examines “the entrepreneurial DNA of 1776,” plus 10 reasons for optimism today. It’s part history lesson, part investment guide and part birthday card to a nation sometimes preoccupied with its problems.

Legacy of innovation

To be sure, many of the issues we face today – polarization, geopolitical threats, economic inequality and rising debt – would trouble founders like George Washington, Alexander Hamilton and Ben Franklin, Quinlan believes. “But they’d be amazed and gratified to see that the American spirit of problem-solving and innovation lives on. Franklin, the original American entrepreneur, would be right at home with artificial intelligence (AI) and biotechnology,” he says.

Reasons to celebrate

Well into the 21st century, the U.S. leads the way in industries as diverse as aerospace, agriculture, finance and health care. “With just 4% of the world’s population, Americans generate roughly a quarter of its GDP1,” Quinlan says. What’s the secret? Here are some of CIO’s 10 reasons to celebrate:

- Geography as a superpower: Energy, minerals, waterways and arable land, plus oceans and allies at its borders, create a huge U.S. geographical edge from sea to shining sea.

- Technological prowess. “Despite China’s astonishing progress in AI2 and other technologies, the U.S. remains the largest market for R&D and innovation,” Quinlan says.

- Creative destruction: Businesses rise and fall quickly, making way for fresh shoots of innovation, with nearly 6 million new business applications just in 2025.3

- Foreign capital: Overseas investors remain bullish on the U.S., currently holding some $50 trillion4 in U.S. Treasurys, corporate bonds, stocks and other assets.

Investing in the next 250 years

“A dynamic, entrepreneurial economy goes hand-in-hand with solid equity returns,” Quinlan says. “U.S. stocks should be a bedrock of portfolio construction, in our view.” Yet creative destruction, while a strength, underscores the importance of diversifying across industries and sectors, with international equities and fixed income for balance. He adds, “Diversification and staying invested through short-term volatility could help position you for potential long-term growth as the U.S. economy embarks on the next era in its remarkable history.”

Read the Capital Market Outlook report for a deeper dive into the economy’s founding and current strengths. And tune in regularly to the latest Market Update audiocast for regular updates on the economy and markets.

1McKinsey & Company, “Sustaining America’s competitive edge,” May 6, 2026.

2The Wall Street Journal, “China Has Matched Anthropic in Cybersecurity, Resetting AI Race,” June 27, 2026.

3Finder.com, “New business statistics: 2005 to June 2026,” Jun 10, 2026.

4U.S. Commerce Department and International Monetary Fund

5Kantar BrandZ, “Most Valuable Global Brands 2026,” 2026.

6Visual Capitalist, “Ranked: The World’s Biggest Reserve Currencies Today,” June 11, 2026.

7QS Quacquarelli Symonds Limited, “QS World University Rankings 2026,” 2026.

Does a 60/40 stock-bond portfolio still make sense?

WHEN STOCKS STRUGGLE, BONDS RALLY. That simple idea has guided generations of investors seeking portfolio diversification. It underpins the classic 60-40 asset allocation formula: 60% stocks for potential growth and 40% bonds for potential stability. But when stocks and bonds start to rise and fall in unison, as they have recently, how can investors find the diversification they require?

A recent Chief Investment Office (CIO) Capital Market Outlook article, “Stock-bond correlations are shifting: What it means for diversification,” examines reasons behind recent rising stock-bond correlations and how investors can respond. “A balanced mix of stocks and bonds remains an essential model for investors seeking potential growth and stability,” says Kirsten Cabacungan, CIO investment strategist and author of the report. “But diversification within that model may now require a more dynamic approach.”

What are stock-bond correlations?

Correlations measure how two asset classes perform relative to one another on a scale from 1 (moving together absolutely) to minus 1 (moving in opposite directions). “Low and negative correlations, which produce more pronounced diversification benefits, have tended to occur in low and stable inflation environments,” Cabacungan explains. “That was the case for much of the past two decades, with bonds cushioning stock drawdowns and helping to stabilize portfolio returns.”

A little history: How and why correlations have changed

“The pandemic era marked an inflection point,” she says. “Following a surge in fiscal and monetary government stimulus, inflation rose to multidecade highs, prompting the Federal Reserve to tighten policy, which pushed interest rates higher and weighed on bond performance at a time when equities were also struggling. In 2022, simultaneous drops in both asset classes led to a 16% drawdown for a 60/40 portfolio1 — the worst annual performance since 2008.

But, as conditions began to stabilize in the years that followed, the 60/40 formula delivered strong returns, up 18% in 2023, 16% in 2024, and 14% in 2025,1 as higher yields and a more stable rate backdrop helped bonds hold up during pockets of equity market volatility. Even so, that progress has been uneven. “Those diversification benefits came under renewed pressure this year, as geopolitical tensions and uncertainty around the Federal Reserve’s policy path coincided with a rise in short-term correlations to their highest levels since 1999,2” Cabacungan says.

What could being diversified look like in today’s markets?

History suggests that when inflation pressures ease, stock-bond diversification benefits can improve over time. “In today’s more complex environment, the goal is not to abandon diversification, but to make it more resilient,” Cabacungan notes.

To help improve diversification in environments of higher correlations, consider:

- A broad array of investments across sectors, geographies and types within each asset class

- Inflation-sensitive assets, such as commodities,

infrastructure, real estate and real assets - Private markets, for qualified investors

The CIO still maintains a bias toward equities over bonds for their growth potential, she points out, but it encourages a more diverse selection of each. “Since not all stocks and bonds behave the same, holding a broad array across sectors, geographies and types within each asset class could help stabilize returns.” For further diversification, investors may also want to consider inflation-sensitive assets such as commodities, infrastructure, real estate and real assets, while qualified investors might explore diversifying through private markets.

For a closer look at what stock-bond correlations could mean for your portfolio, read the Capital Market Outlook article. And tune in regularly to the latest Market Update audiocast from the Chief Investment Office for updates on the economy, markets and inflation.

1Chief Investment Office calculations. FOR INFORMATIONAL PURPOSES ONLY. A 60/40 allocation assumes a 60% allocation to the S&P 500 Total Return Index and 40% to the Bloomberg U.S. Aggregate Bond Total Return Index, rebalanced annually. Data reflects the period from 1990-2025. Performance of 60/40% Allocation is intended to illustrate the effect of asset allocation and diversification. It is not an advertisement or representation of any investment advisory products or services offered by Merrill. Results shown are based on an index and are illustrative; they assume reinvestment of income and no transaction costs or taxes. Indexes are unmanaged. Direct investment cannot be made in an index. Past performance is no guarantee of future results.

2Stocks represented by the S&P 500 Total Return Index. Bonds represented by the Bloomberg U.S. Aggregate Bond Total Return Index. Bloomberg. Data as of May 27, 2026.

Rates hold firm, for now, under new Fed chair

IN KEVIN WARSH’S FIRST MEETING AS FED CHAIR, the Federal Reserve (the Fed) on June 17 held the federal funds rate steady at 3.50% to 3.75%. The decision dashed any hopes that a change in leadership might prompt immediate rate-cutting and signaled that inflation is at least as big a concern for the Fed right now as stimulating economic growth. Just a week earlier, May’s Consumer Price Index (CPI) showed the annual inflation rate climbing above 4% for the first time in three years.1

What’s behind the Fed rate decision?

“Conditions have shifted from the start of the year, when two cuts for 2026 seemed likely,” says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank. The Iran war spiked energy costs and pushed prices for other goods higher, and the U.S. economy has shown remarkable resilience, adding 172,000 jobs in May.2 Equity markets, despite heightened volatility, continue to find new highs, and long-term bond yields have risen amid investor concerns over the Middle East and inflation.3

When could we see a rate cut?

The administration supported Warsh as likelier than his predecessor, Jerome Powell, to push for lower rates,4 which make borrowing easier and tend to stimulate hiring. Yet sticky inflation generally prompts the Fed to do the opposite, raising rates to slow the economy. “BofA Global Research now foresees no new rate cuts until at least mid-2027, and the chances of a .25% increase in the next year have grown,” Hyzy says. “Moving forward, new economic data will be the most important factor as the Fed balances its dual mandates of full employment and stable inflation.”

How can you respond to periodic volatility?

May’s healthy jobs numbers, while good news for workers and the economy, helped drive a 2.6% drop in the S&P 500 index on June 5 as hopes of a rate cut diminished.5 “Investors should expect that sort of choppiness over the next few months,” Hyzy believes. “Yet the job gains, spread across healthcare, logistics, financial services, hospitality and leisure and other industries, reflect strong economic fundamentals,” Hyzy adds. “Stay diversified and consider viewing short-term volatility as a potential opportunity to strategically add to your portfolio,” he suggests.

For bond investors, higher yields offer the potential for meaningful income. “Instead of trying to predict exactly when interest rates and yields may change, explore adding bond duration gradually and emphasizing quality,” Hyzy says. Investors concerned about inflation might consider Treasury Inflation-Protected Securities (TIPS), while high-income investors concerned about taxes may find income opportunities with tax-advantaged municipal bonds.

Check back here for updates, and tune in regularly to the Market Update audiocast from the Chief Investment Office as interest rates and inflation data evolve.

1CNBC, Consumer prices rose 4.2% annually in May, highest in three years

2The Wall Street Journal, “May jobs growth puts U.S. on a strong hiring streak,” June 5, 2026.

3CNBC, “Treasury yields edge higher as traders weigh rate outlook, fresh Iran tensions,” June 8, 2026.

4CNBC, “Kevin Warsh sworn in as Fed chair as Trump seeks interest rate cuts,” May 22, 2026.

5The New York Times, “Stocks slide as investors see rates rising after strong jobs data,” June 5, 2026.

In a year of surprises, what comes next?

AN UNEXPECTED GEOPOLITICAL CONFLICT, A QUICK NASDAQ MARKET CORRECTION, concerns over sticky inflation in the U.S. “With all the tumult, investors are now wondering, “What comes next?” says Chief Investment Officer Chris Hyzy.

He and his team at Merrill and Bank of America Private Bank’s Chief Investment Office (CIO) address that question and many more in the upcoming 2026 Midyear Outlook webcast, “Shifting gears: New drivers of potential market expansion.”

The video above offers a quick refresher of the events that have shaped the investment landscape so far this year and a preview of what could drive the markets over the second half of the year and beyond. Watch it, then save the date to get the full story when the webcast premieres on June 23 at 2 P.M. (ET).

Who’s featured

In the webcast, Hyzy will be joined by BofA Global Research’s head of U.S. Equity and Quantitative Strategy Savita Subramanian and head of U.S. Economics Research Aditya Bhave, as well as the CIO’s head of Portfolio Strategy Marci McGregor, head of Market Strategy Joe Quinlan and head of Cross-Asset Market Strategy Matthew Diczok.

Your questions answered

They’ll share their thoughts on continuing geopolitical unrest, inflation’s impact on bond yields and equity prices, whether artificial intelligence is still a potential growth opportunity, the effect of the midterms on the markets, and what strategies you can consider for the rest of the year. In the meantime, see if you can answer the questions below.

Test your Midyear Market Knowledge

True or false: Just two AI-related stocks make up about half of the S&P 500’s 9.8% year-to-date return.

Choose your answer and tap + to learn more

True or false: The S&P 500 has not experienced a 10% pullback since April 2025.

Choose your answer and tap + to learn more

The biggest oil shock: Market resilience

LATEST TALKS BETWEEN IRAN AND THE U.S., if they succeed, could lead to a welcome opening of the Strait of Hormuz. The shutdown has caused history’s greatest oil disruption, affecting some 20% of the world’s supply.1 So, how has the world thus far avoided an economic crisis? “While higher oil prices and inflation are creating real pain for millions of consumers, several factors have helped to limit its global impact so far,” says Ariana Chiu, investment strategist in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank.

Which countries are most affected by the oil disruption?

“A robust economy and energy self-sufficiency are supporting U.S. economic stability in the face of the Hormuz oil shock,” Chiu says. Asia, which accepts more than 80% of the oil that moves through the Strait of Hormuz,2 and Europe, which sources much of its jet fuel via the passageway, are feeling the brunt, she adds. Yet the global economy has shown surprising resilience, thanks to several forces that together are mitigating about half of the disrupted supply. A recent CIO Capital Market Outlook report, “No two oil shocks are created equal,” explores those forces as well as the risks that could lead to a wider economic crisis.

What has limited its global impact so far?

Chiu points to five key factors helping the global economy weather the oil disruption:

- A prewar “super glut.” Robust 2025 production created an oil oversupply of about 3 million barrels per day at the outset of the conflict.3

- Rerouting. While the Strait of Hormuz remains a key oil conduit, exporters have offset about 5 million barrels a day using alternative pipelines and ports,4 Chiu says.

- Strategic reserve releases. In March, 32 Organisation for Economic Co-operation and Development (OECD) nations agreed to release 400 million barrels of strategic petroleum reserves.5

- Lower consumption. Global oil use dropped by about 2.3 million barrels per day in April, year over year.6 “As gas prices rise, Asian governments in particular have recommended consumers take fewer business trips, work remotely and leverage alternative forms of transportation,” Chiu says.

- U.S. economic and energy resilience. As a net oil exporter, the U.S. is helping to fill the Hormuz gap, with exports rising sharply since the war started to over 6 million barrels per day.7

Moves for investors to consider

“For now, financial markets continue to price in a relative de-escalation in the coming months. But the longer the disruption lasts, the greater the risk of a larger hit to economic growth,” says Chiu. “For investors, we continue to prefer the U.S. in portfolios because of its ability to remain resilient versus other economies.”

Focus on the U.S.: An emphasis on high-quality U.S. stocks may offer a buffer from oil shocks, given U.S. energy self-sufficiency, while also positioning investors to potentially benefit from U.S. economic strength, record earnings growth and artificial intelligence capital expenditures in the long term. That said, it’s important to stay disciplined and diversified across and within asset classes in the face of potentially volatile headlines, Chiu adds, and to rebalance during periods of volatility.

For latest insights from the CIO on the Iranian conflict and its impact on the economy and markets, tune in to the Market Update audiocast.

1CNBC, “The U.S.-Iran war is the biggest oil disruption in history,” March 9, 2026

2U.S. Energy Information Administration, “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint,” June 16, 2025.

3International Energy Agency, “Oil market report,” Jan. 21, 2026.

4International Energy Agency, “Oil market report,” March 12, 2026.

5International Energy Agency, “IEA Member countries to carry out largest ever oil stock release amid market disruptions from Middle East conflict,” March 11, 2026.

6International Energy Agency, “Oil market report,” April 14, 2026.

7Bloomberg, US oil exports hit record as Iran War energy crunch deepens,” April 29, 2026.

Interest rates: Up, down or flat under new Fed chair?

EVEN AS LEADERSHIP OF THE FEDERAL RESERVE (the Fed) changes hands, persistent inflation may eliminate chances of hoped-for interest rate cuts through 2026. Kevin Warsh, confirmed by the full Senate on May 13, replaces Jerome Powell, whose term as chair ends on May 15. While the administration backed Warsh, a so-called interest rate dove favoring lower rates, as potentially more aggressive than his predecessor in pushing for cuts,1 April inflation figures released yesterday show the Consumer Price Index up 3.8% from a year ago, well above the Fed’s 2% target.2

The case for current rate inaction

The latest inflation figures clearly present a challenge for the new Fed chair. Markets welcome interest rate cuts because they stimulate hiring and economic growth and make it easier for businesses and consumers to borrow money. “Yet while the labor market has softened, we haven’t seen an increase in recent layoffs,” says Matthew Diczok, head of Cross-Asset Market Strategy for the Chief Investment Office (CIO). “For the time being, this labor stability enables the Fed to focus on inflation pressures related to energy price spikes from the Iran conflict and tariff uncertainties, rather than unemployment.”

Warsh would need to rally six other Fed governors to vote for a rate cut — a difficult task as long as these conditions persist, he adds. “Markets, in fact, no longer expect rate cuts this year. That’s not necessarily a bad thing, as it highlights continuing economic resilience. Should inflation slow, as expected, it likely just pushes rate cuts into 2027.” BofA Global Research, which had anticipated two cuts in 2026, now believes cuts may not come until mid or late 2027. A rate hike this year is considered unlikely.

The case for future cuts in the Warsh era

While interest rate expectations are always subject to change as economic conditions evolve, rising U.S. economic productivity may allow the Fed to accommodate an extended era of somewhat elevated inflation while maintaining or lowering interest rates to spur growth. Diczok points to the early 1990s, when the Fed allowed inflation to hover around 3.3% amid a tech-related productivity boom.

Today, productivity gains from artificial intelligence (AI) and other technologies are outpacing wage growth and supporting strong equity market performance, Diczok notes. “If productivity gains continue and we are able to work through the current energy crisis and get past tariff uncertainties, that would support the Fed’s ability to resume rate cuts next year.”

In the meantime, he adds, “fixed income investors with excess cash could consider longer term bonds.” In fact, he says, “even short-term maturities don’t look bad right now.” Relative to the rest of the world, U.S. Treasurys and Treasury Inflation-Protected Securities (TIPS) offer attractive inflation-adjusted yields and fixed income.

For latest insights on the markets, economy and where interest rates might go next, tune in regularly to the CIO’s Market Update audiocast.

Important Disclosures

Investing involves risk, including the possible loss of principal. Past performance is no guarantee of future results.

Asset allocation, diversification and rebalancing do not ensure a profit or protect against loss in declining markets.

Opinions are as of the date of these articles and are subject to change.

Bank of America, Merrill, their affiliates, and advisors do not provide legal, tax, or accounting advice. Clients should consult their legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., (“Bank of America") and Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S" or “Merrill"), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”).

BofA Global Research is research produced by BofA Securities, Inc. (“BofAS”) and/or one or more of its affiliates. BofAS is a registered broker-dealer, Member SIPC, and wholly owned subsidiary of Bank of America Corporation.

All recommendations must be considered in the context of an individual investor’s goals, time horizon, liquidity needs and risk tolerance. Not all recommendations will be in the best interest of all investors.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration.

Investments in foreign securities involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

Income from investing in municipal bonds is generally exempt from Federal and state taxes for residents of the issuing state. While the interest income is tax-exempt, any capital gains distributed are taxable to the investor. Income for some investors may be subject to the Federal Alternative Minimum Tax (AMT).

Retirement and Personal Wealth Solutions is the institutional retirement business of Bank of America Corporation (“BofA Corp.”) operating under the name “Bank of America.” Investment advisory and brokerage services are provided by wholly owned non-bank affiliates of BofA Corp., including Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as "MLPF&S" or "Merrill"), a dually registered broker-dealer and investment adviser and Member SIPC. Banking activities may be performed by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A., Member FDIC.

You have choices about what to do with your 401(k) or other type of plan-sponsored accounts. Depending on your financial circumstances, needs and goals, you may choose to roll over to an IRA or convert to a Roth IRA, roll over a 401(k) from a prior employer to a 401(k) at your new employer, take a distribution, or leave the account where it is. Each choice may off er different investments and services, fees and expenses, withdrawal options, required minimum distributions, tax treatment (particularly with reference to employer stock), and provide different protection from creditors and legal judgments. These are complex choices and should be considered with care.

Diversification does not ensure a profit or protect against loss in declining markets.

Sustainable and Impact Investing and/or Environmental, Social and Governance (ESG) managers may take into consideration factors beyond traditional financial information to select securities, which could result in relative investment performance deviating from other strategies or broad market benchmarks, depending on whether such sectors or investments are in or out of favor in the market. Further, ESG strategies may rely on certain values based criteria to eliminate exposures found in similar strategies or broad market benchmarks, which could also result in relative investment performance deviating.

Investing in Gold involves special risks, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes, and the impact of adverse political or financial factors.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investments focused in a certain industry or sector may pose additional risks due to lack of diversification, industry volatility, economic turmoil, susceptibility to economic, political or regulatory risks and other sector concentration risks.