Most heirs face many complex decisions — and potential tax consequences. These insights can help you avoid common mistakes and make more informed choices.

“Don’t wait until the decisions are urgent. Discuss in advance how the gift could help you pursue your goals.”

AN INHERITANCE CAN SEEM LIKE a mixed blessing, coming as it often does after the loss of a loved one. At such an emotional time, it can be difficult to think through what you need to do to manage the gift. But even if your parents decide to give you your inheritance or a portion of it while they’re still living — as parents increasingly prefer to do — you’ll likely have many questions, says Jason Albano, managing director, wealth strategies executive with Bank of America Private Bank.

If you expect to receive an inheritance at some point in your life, your financial advisor can provide useful guidance, he notes. “Don’t wait until the decisions are urgent. Discuss in advance potential tax consequences with your advisor and personal tax professional and how the gift could help you pursue your goals,” Albano adds. You might also want to talk with your parents about their hopes for your financial future — even how they might be planning to structure their future gift to you. Read the insights below for a better sense of how to prepare for the many issues heirs can face.

A: It’s not necessary to ask how much money your parents might leave you. “Start the conversation by asking about their values and what wealth means to them,” suggests Merrill Lynch Wealth Management Advisor Todd Silaika. That can lead to productive conversations about the role an inheritance could play in your financial future and what your parents’ expectations might be. This sort of conversation also provides you with the opportunity to share your preferences and priorities. For instance, if there’s a family business or even a family vacation home and you have no interest in owning either, be upfront about that. “When everyone understands the expectations, the outcomes tend to be better for everyone,” Silaika notes.

A: You’ll likely have some time before you receive the funds. Depending on the complexity of the estate, the probate process, if applicable, generally takes at least six months to a year. And that’s usually for the best, says Private Wealth Advisor Cheryl Smith. Too often, beneficiaries make large purchases or sweeping decisions they later regret. Even paying off debt right away may not be in your best interests, says Albano. “Does it make sense to pay off a mortgage at a rate below 3%? You might do better than a 3% return elsewhere,” he notes.

Instead, consider setting up a meeting with your advisor to discuss your competing goals and how you could manage your newfound wealth to help you pursue them. Albano suggests looking at four buckets — spending needs, short-term goals, long-term goals and philanthropy. “How you allocate your inheritance to these buckets depends on your situation,” he says. If you have young children, a portion could go toward college costs in the long-term bucket. But if you’re looking at renovating your home or relocating, you’ll probably want to put those funds into a short-term bucket and make sure they’re easily available.

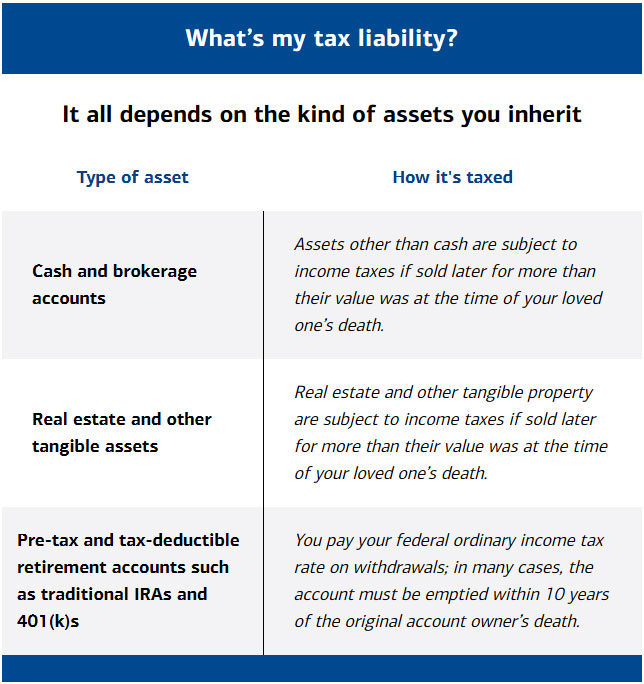

A: Most inheritances aren’t, says Albano. You might be named the beneficiary of a retirement account — or you could inherit the family home, for instance. If you’ve inherited a tax-deferred account like an IRA or a 401(k) account and you’re an eligible designated beneficiary1 or designated beneficiary, you may have as long as 10 years after the death of the original account owner to fully liquidate the account (depending on your age relative to the original account owner and certain other circumstances). The rules are complex, and distributions have tax implications. You should consult your tax professional regarding your specific situation. You’ll also be responsible for taking required minimum distributions (RMDs) as provided in the federal tax code. Assets in taxable accounts, by contrast, can be either liquidated or left in the account indefinitely. Again, you’ll want to meet with a tax professional to decide your best strategy.

“Things can get more complicated when converting real assets, such as a family home or business, into cash, especially when multiple beneficiaries are involved,” notes Albano. If there are disputes over a will, it could take years for the issues to be resolved. In the best-case scenario, parents have worked with their advisor and estate attorney to construct a will or trust in such a way that its provisions account for the beneficiaries’ desires — for instance, which child wants to keep the family home or work in the family business.

A: For tax purposes, an inheritance generally isn’t considered income, but there are some exceptions. Typically, the estate will pay any estate tax owed, with the beneficiaries receiving assets from the estate free of income taxes (see exception for retirement assets in the chart below). As a beneficiary, if you later sell or earn income from inherited assets, there may be income tax consequences. And if you inherit certain tax-deferred accounts like a traditional IRA or 401(k) account, you’ll pay taxes on your withdrawals, including RMDs, as ordinary income at whatever your tax rate is. Also, some states have an inheritance tax.

When it comes to taxable accounts and other assets like real estate, there’s the possibility you’ll owe no income tax because the cost basis of the asset gets stepped up (or down) to the current fair market value upon its owner’s death, thereby wiping out any taxable capital gains on appreciated assets, says Albano. Keep in mind that if you inherit an asset that provides income — say, a trust that pays out annually — it may put you in a higher marginal tax bracket.

A: Whenever your net worth changes, or you have a significant life event, you should take the time to review your estate plan and make appropriate changes, says Albano. You may need to consider how to protect certain newly acquired assets — for instance, a family home or business that’s been passed down to you that you want someday to go to your children.

“Ask yourself, if something happens to you, how will your assets flow to the people you care about?” he adds. A trust might be one way to accomplish that aim. Then talk to your advisor about how you might want to use your inheritance to further your own legacy — and help make your beneficiaries’ futures more secure.

¹ An eligible designated beneficiary (EDB) is a surviving spouse, disabled or chronically ill individual, an individual who is not more than 10 years younger than the decedent, or a minor child of the account owner. Distribution rules differ based on the date of death, whether the beneficiary is an EDB and whether the original account owner died before or after their beginning date for required minimum distributions.

Trust, fiduciary, and investment management services are provided by Bank of America Private Bank, a division of Bank of America, N.A. and its agents, Member FDIC, and a wholly owned subsidiary of Bank of America Corporation.

Timely insights to stay ahead of the curve