The recent rapid rise in home prices may have affected the equity you have in your home. Here’s how to figure out how much you have — and how to make the most of it.

THE AVERAGE HOME PRICE IS UP SHARPLY over the past five years, and you may be sitting in an asset with a very different value than it had when you first moved in. As of the third quarter of 2025, total equity for homeowners with mortgages reached $17.1 trillion, according to the real estate analytics firm Cotality; for the average U.S. homeowner, that amounts to roughly $299,000 in accumulated equity.1

Increasing home values can present a valuable opportunity for many homeowners. “Any financial plan has to include access to liquidity,” says Paul Rua, credit and banking product executive at Bank of America. “Home equity offers that.”

So understanding how to calculate your equity — and how banks view it — is critical, especially if you want to borrow money against that equity to pay for a home improvement project, cover emergency expenses, help pay for your child’s college tuition or reach some other financial goal. Your home’s equity could also affect certain borrowing costs and determine which financing options may be available to you.

When considering whether you should use your equity for a certain expense, a good litmus test is whether it improves your finances or makes your life better, Rua says. For example, using equity to pay for education could increase a student’s earning potential, while home improvements could improve your living conditions, if, say, “you’re expanding your home for a growing family or making room for aging parents,” he adds.

In some cases, debt consolidation may be a smart use of home equity — provided you’re comfortable that you won’t run the debt back up again. For lenders, loans secured by real estate are typically less risky than other types of debt. As a result, they tend to carry lower interest rates. “Home equity continues to be a very competitive way to borrow money compared with other types of credit, such as unsecured debt or credit card debt,” Rua adds.

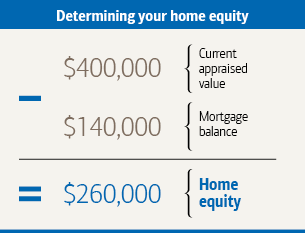

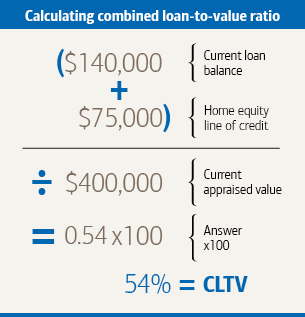

Before you make any plans to take advantage of what you hope is a larger pool of equity, start with a baseline calculation. You can figure out how much equity you have in your home by subtracting the amount you owe on all loans secured by your house from its current value, which you can determine with a formal appraisal or simply estimate using online tools. Your total loans include your primary mortgage as well as any home equity loans or unpaid balances on home equity lines of credit (HELOCs). In this example of a typical homeowner, Caroline owes $140,000 on a mortgage for her home, which was recently appraised at $400,000.

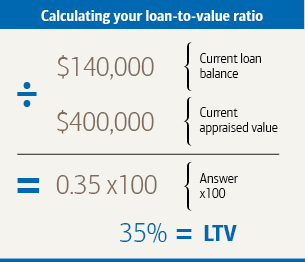

Mortgage providers may use additional calculations when deciding how much they’re willing to lend you — or even whether they’re willing to lend to you at all. One measure they use is the loan-to-value (LTV) ratio. When you first apply for a mortgage, this number reflects the amount of the loan you’re seeking relative to the home’s value. Once you own a home and have a mortgage, your LTV ratio is based on your loan balance. Your LTV ratio can affect whether you might be able to use your home to secure a loan.

With a higher LTV ratio, banks may consider your loan higher risk, which can increase your borrowing costs. A professional appraisal is key to accurately figuring out your LTV ratio. That’s why your lender often will require an on-site appraisal as part of the process for obtaining a loan. To figure out your LTV ratio, divide your current loan balance (you can find this number on your monthly statement or online account) by your home’s appraised value. Multiply by 100 to convert this number to a percentage. In the example at left, Caroline’s loan-to-value ratio is 35%.

If you’re considering a home equity loan or a HELOC, another important calculation is your combined loan-to-value (CLTV) ratio. Your CLTV ratio compares the value of your home with the combined total of the loans your home secures, including the loan or line of credit you’re seeking. Say Caroline wants to apply for a $75,000 home equity line of credit. She calculates what her CLTV ratio would be if she were approved for it, and since most lenders require your CLTV ratio to be below 85% to qualify for a home equity line of credit, Caroline likely would be eligible.

While home equity can be a valuable financial resource, you should keep some potential drawbacks in mind. “Home equity loans have been impacted by recent interest rate trends,” Rua says. A higher interest rate environment means borrowing today could cost you more than it may when interest rates go back down. Also, if your loan has an adjustable rate, your payments could rise and fall over time, making payments less predictable.

Finally, if you’re unable to pay back your home equity loan, your house could be at risk of foreclosure. “Anytime we're spending our home equity, we need to be thoughtful about it,” Rua says. “It is not an ATM to haphazardly use, but it is a very important tool to have in your toolbox.” Your financial advisor can help you determine whether tapping your home equity is the right move for you.

Smart home improvements can help increase your home’s value too. However, it’s a good idea to consult an appraiser or real estate professional before investing in any renovations. Remember that economic conditions — and the normal dips and swings of the real estate market — can affect your home’s value no matter what you do. If the value of your home increases due to a renovation project, your LTV ratio could drop, depending on how much equity you tapped to cover the costs. But falling home prices in your area could cancel out the value of any improvements you might make.

Building up equity in your home can help you pursue other important goals and provide a financial buffer in case of emergencies. The first step to taking advantage of it is knowing how much you have.

Work one-on-one with a Merrill advisor for more insights and personalized guidance. Connect with us today.

1Cotality, “Homeowner Equity Report” – Q3 2025, accessed February 12, 2026.

HELOC funds may not be used to purchase, carry or trade securities or repay debt incurred to purchase, carry or trade securities.

Banking, mortgage and home equity products offered by Bank of America, N.A., and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America Corporation. Equal Housing Lender ![]() . Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice.

. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice.

Timely insights to stay ahead of the curve